All Categories

Featured

Table of Contents

Maintaining your classifications up to day can make certain that your annuity will be taken care of according to your wishes need to you pass away suddenly. A yearly testimonial, major life occasions can prompt annuity proprietors to take one more appearance at their recipient selections.

As with any type of economic item, seeking the assistance of a financial consultant can be helpful. A financial coordinator can direct you via annuity monitoring processes, consisting of the techniques for upgrading your agreement's beneficiary. If no beneficiary is called, the payment of an annuity's survivor benefit goes to the estate of the annuity owner.

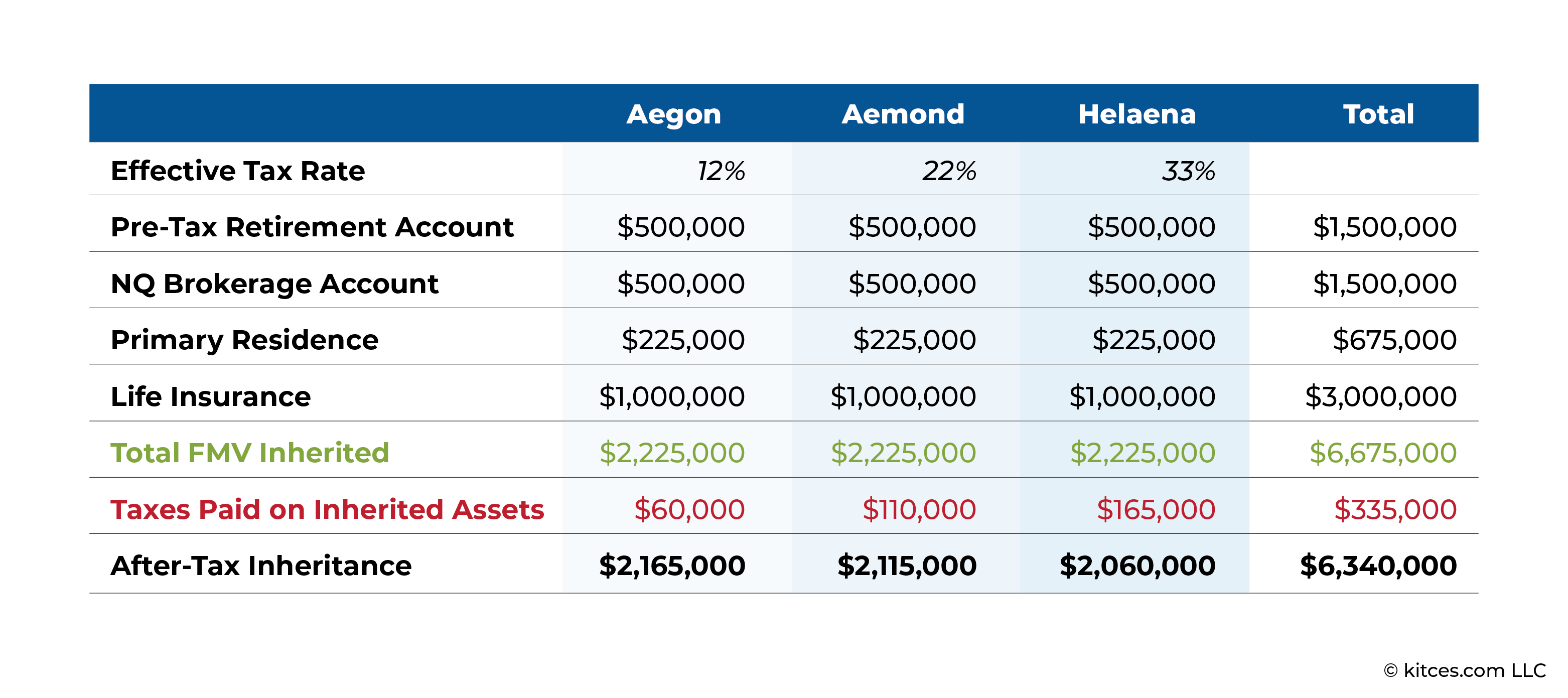

Acquiring an annuity can be a fantastic windfall, however can additionally elevate unexpected tax obligation obligations and management problems to manage. In this post we cover a few basics to be familiar with when you inherit an annuity. Recognize that there are 2 kinds on annuities from a tax obligation point of view: Qualified, or non-qualified.

When you take money out of an acquired qualified annuity, the total withdrawn will certainly be counted as taxable revenue and taxed at your normal earnings tax price, which can be quite high depending upon your financial scenario. Non-qualified annuities were funded with cost savings that currently had tax obligations paid. You will not owe tax obligations on the initial cost basis (the overall contributions made originally right into the annuity), but you will certainly still owe taxes on the development of the investments nevertheless which will certainly still be exhausted as revenue to you.

Particularly if the initial annuity proprietor had actually been receiving repayments from the insurance policy company. Annuities are usually made to offer revenue for the initial annuity proprietor, and after that cease payments once the original owner, and perhaps their partner, have passed. Nevertheless, there are a couple of scenarios where an annuity might leave a benefit for the beneficiary acquiring the annuity: This implies that the initial owner of the annuity was not receiving regular repayments from the annuity yet.

The beneficiaries will have numerous choices for how to get their payout: They might maintain the money in the annuity, and have the properties relocated to an inherited annuity account (Guaranteed annuities). In this case the properties might still stay invested and continue to grow, nonetheless there will be required withdrawal rules to be knowledgeable about

How is an inherited Multi-year Guaranteed Annuities taxed

You may additionally be able to cash out and get a lump amount payment from the inherited annuity. However, be certain you understand the tax effects of this decision, or talk with an economic expert, due to the fact that you might be subject to substantial income tax obligation responsibility by making this political election. If you choose a lump-sum payout choice on a certified annuity, you will certainly based on income taxes on the whole worth of the annuity.

An additional attribute that may exist for annuities is an assured survivor benefit (Annuity payouts). If the initial owner of the annuity chosen this feature, the recipient will certainly be qualified for an one time round figure benefit. How this is exhausted will depend on the sort of annuity and the value of the survivor benefit

.jpg)

The details regulations you must follow rely on your connection to the individual that passed away, the kind of annuity, and the phrasing in the annuity contract sometimes of purchase. You will certainly have a collection amount of time that you should withdrawal the assets from the annuity after the initial proprietors fatality.

Due to the tax obligation repercussions of withdrawals from annuities, this indicates you require to carefully intend on the very best way to withdraw from the account with the most affordable quantity in tax obligations paid. Taking a big round figure may press you right into really high tax brackets and lead to a bigger section of your inheritance mosting likely to pay the tax costs.

It is additionally vital to recognize that annuities can be traded. This is known as a 1035 exchange and enables you to relocate the cash from a certified or non-qualified annuity into a various annuity with one more insurance provider. This can be an excellent option if the annuity contract you inherited has high fees, or is just not best for you.

Handling and investing an inheritance is unbelievably important role that you will be pushed into at the time of inheritance. That can leave you with a whole lot of questions, and a great deal of possible to make pricey mistakes. We are here to assist. Arnold and Mote Wide Range Monitoring is a fiduciary, fee-only financial organizer.

Do you pay taxes on inherited Fixed Income Annuities

Annuities are one of the numerous devices financiers have for building wealth and safeguarding their economic wellness. An acquired annuity can do the same for you as a recipient. are agreements in between the insurance provider that issue them and the people who buy them. Although there are different types of annuities, each with its very own advantages and features, the vital aspect of an annuity is that it pays either a series of payments or a lump amount according to the contract terms.

If you recently acquired an annuity, you might not recognize where to start. That's entirely understandablehere's what you need to understand. In enhancement to the insurance provider, several parties are associated with an annuity contract. Annuity owner: The individual who participates in and spends for the annuity agreement is the proprietor.

The owner has full control over the agreement and can transform beneficiaries or end the agreement subject to any type of appropriate surrender charges. An annuity might have co-owners, which is often the case with partners. Annuitant: The annuitant is the person whose life is used to establish the payment. The owner and annuitant might coincide individual, such as when somebody purchases an annuity (as the proprietor) to offer them with a settlement stream for their (the annuitant's) life.

Annuities with multiple annuitants are called joint-life annuities. As with numerous owners, joint-life annuities are a common framework with couples since the annuity proceeds to pay the making it through spouse after the first partner passes.

When a death benefit is set off, settlements might depend in part on whether the proprietor had already started to obtain annuity settlements. An acquired annuity fatality advantage works differently if the annuitant had not been already getting annuity payments at the time of their passing away.

When the benefit is paid out to you as a round figure, you obtain the entire amount in a solitary payment. If you choose to get a payment stream, you will have several alternatives readily available, relying on the agreement. If the owner was already obtaining annuity payments at the time of death, after that the annuity contract may merely end.

{kind=link}

Table of Contents

Latest Posts

Decoding What Is A Variable Annuity Vs A Fixed Annuity A Closer Look at How Retirement Planning Works What Is Pros And Cons Of Fixed Annuity And Variable Annuity? Advantages and Disadvantages of Diffe

Breaking Down Fixed Vs Variable Annuity Key Insights on Fixed Annuity Vs Equity-linked Variable Annuity Breaking Down the Basics of Fixed Interest Annuity Vs Variable Investment Annuity Benefits of De

Understanding Financial Strategies Everything You Need to Know About Deferred Annuity Vs Variable Annuity Defining the Right Financial Strategy Advantages and Disadvantages of Fixed Interest Annuity V

More

Latest Posts